Apartment living entails a number of shared responsibilities, such as maintaining lifts and managing common funds. However, one question perplexes even the most experienced Management Committee: Does income tax have to be paid by housing societies? What, if anything?

This blog explains India’s income tax laws for RWAs and housing societies in a way that residents and MC members can finally understand by using real-world examples, court decisions, state-specific variations, and simplified language.

Table of Contents

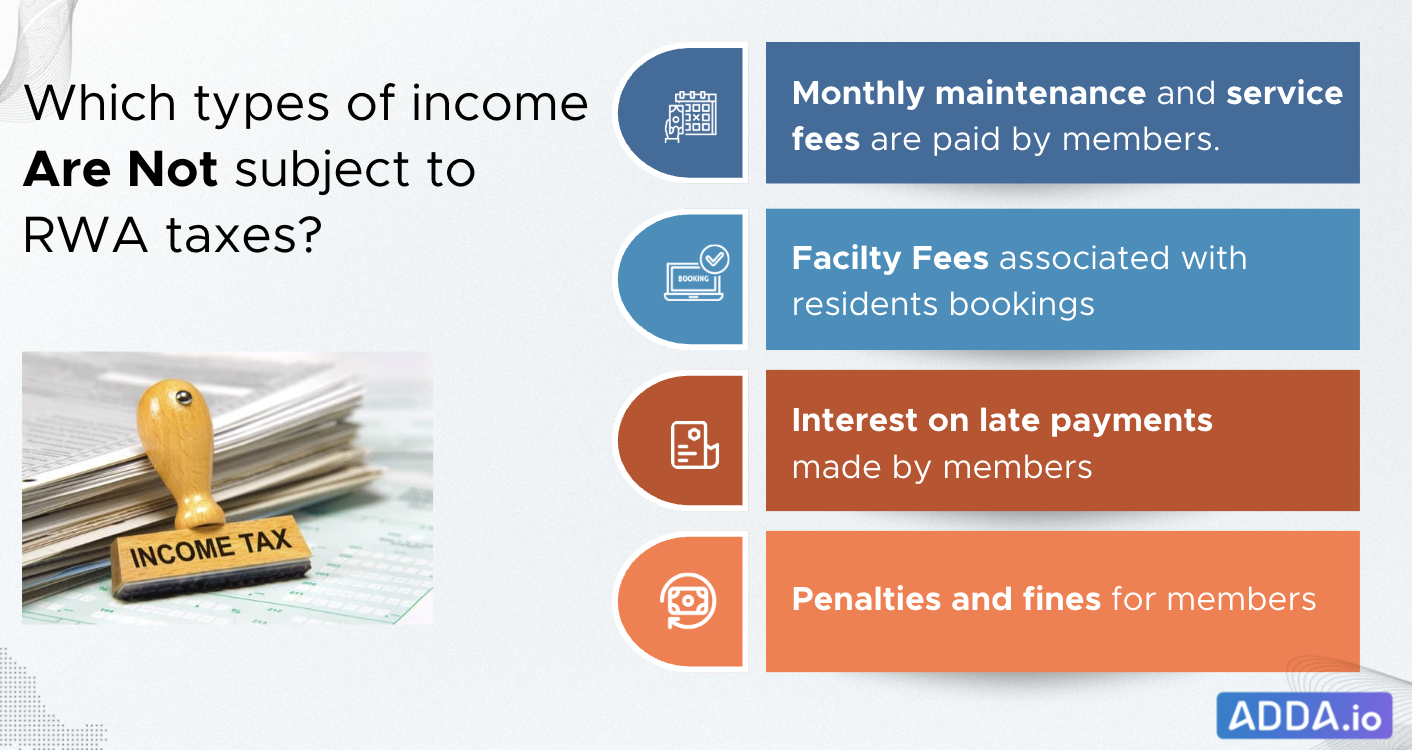

Which types of income are not subject to RWA taxes?

Monthly maintenance and service fees are paid by members.

Fees collected from residents for upkeep, repairs, or security are exempt under the mutuality doctrine.

The Supreme Court ruled in Venkatesh Premises Co-op Society Ltd vs. ITO (2018) that this money is a pooled contribution used for self-benefit rather than income.

Fees associated with residents using the facility

If these fees, like clubhouse reservations, are collected from members and utilised for group activities, they are tax-exempt.

Interest on late payments made by members

This is a compensatory payment made by members, not revenue from third parties. According to the Bombay High Court, this kind of income is still covered by the mutual framework.

Penalties and fines for members

Even if they are punitive in nature, these are not taxable if they are collected from residents and utilised for community operations.

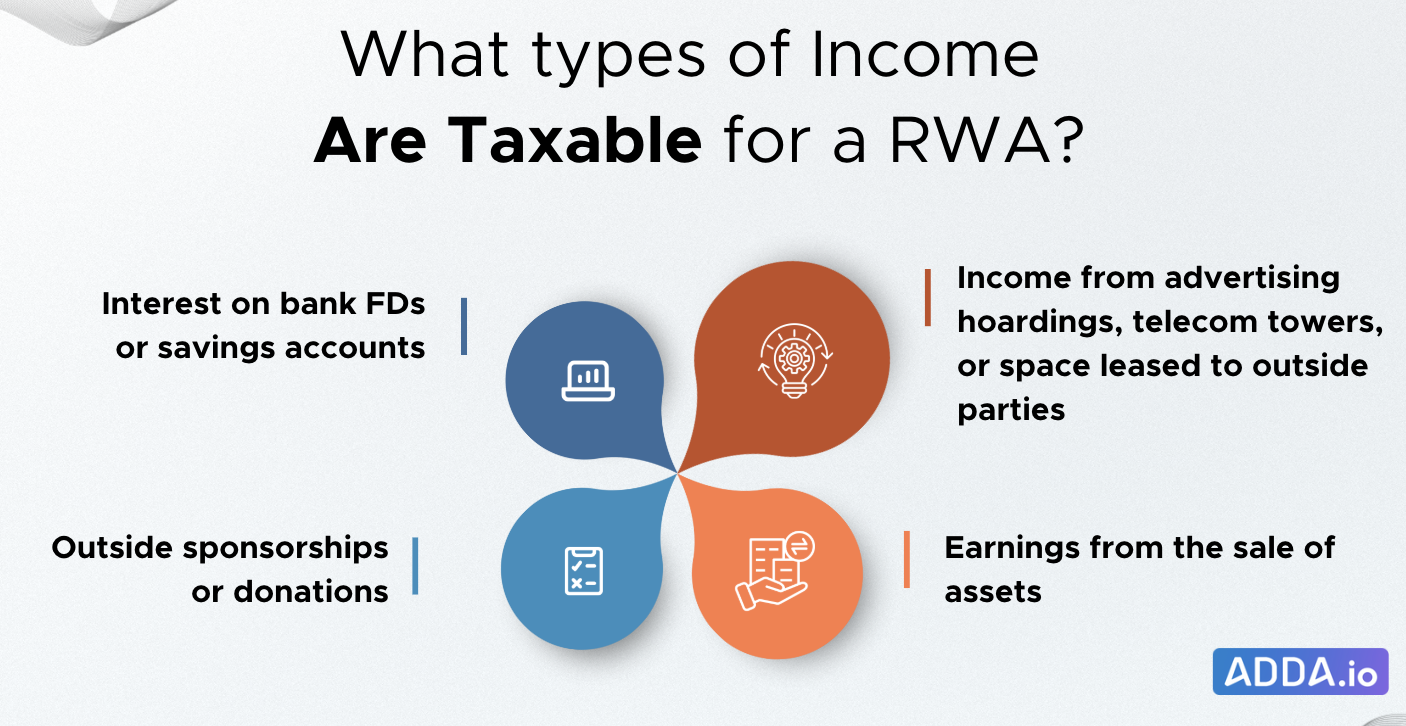

What types of income are taxable for a RWA?

Interest on bank FDs or savings accounts (unless they are in a cooperative bank)

Bangalore Club v. CIT (2013) made it clear that interest from non-member sources, like banks, violates mutuality. It is taxable under “Income from Other Sources.”

Income from advertising hoardings, telecom towers, or space leased to outside parties

Since it originates from outside companies, this is taxable. Mutuality does not apply here.

Outside sponsorships or donations

Even if funds are used for community projects, all income received by commercial or political organizations is liable to full taxation unless otherwise exempted.

Earnings from the sale of assets

It is necessary to report and pay the relevant taxes on the proceeds from the sale of old machinery, generators, or fixtures.

How Do AOA and CHS Get Taxed?

1. Co-operative Housing Society (CHS):

- Usually found in Maharashtra, Gujarat, and other states.

- State-specific registration under the Cooperative Societies Act.

- Treatment of taxes:

- qualified to receive a Section 80P deduction for interest received from cooperative banks.

- Depending on total income, flat slab rates of 10%, 20%, and 30% are applied to taxes.

- Investment income compliance is made easier if funds are held in cooperative institutions.

2. Apartment Owners Associations (AOA) or Resident Welfare Associations (RWA).

- Common in Karnataka, Tamil Nadu, Delhi, and other places – registered under the Societies Registration Act or Apartment Ownership Act.

- Treatment of taxes:

- Ineligible for Section 80P benefits (unless co-op registration is also held).

- The association is required to pay taxes if its annual income, such as interest or rent, surpasses ₹2.5L.

- Depending on the legal structure, it could be taxed at the Maximum Marginal Rate (MMR) or individual slab rates and treated as an Association of Persons (AOP).

What’s the Difference Between “Known” and “Unknown” Member Shares?

Only when a flat owners association is taxed as an AOP does this matter.

Known Shares (Most Common Scenario)

- According to Apartment Ownership Acts, this is the default for AOAs that are registered.

- The majority of apartments today, have clearly defined ownership shares for each unit, which are based on factors like super built-up area, undivided land share (UDS), or flat size.

- In these situations, income tax is computed using standard slab rates, just like personal taxes.

In rare instances, shares that are unknown or indeterminate

This typically occurs when:

- The association lacks clear ownership records or is not formally registered.

- In old, unstructured societies, for example, members have unequal rights that are not explicitly stated in writing.

The IT Department may use the Maximum Marginal Rate, which is the highest tax rate, in these uncommon circumstances.

Important Note: State laws determine whether your association is eligible to be an AOA or CHS. In Maharashtra, you must register as a CHS.

- You must register in Karnataka under the Apartment Ownership Act rather than the Societies Act.

- In Tamil Nadu, registration is typically conducted in accordance with the 1994 Tamil Nadu Apartment Ownership Act.

- The structure is determined by state law based on the location of your flat; you are not free to choose between CHS and AOA.

What are Housing Societies’ precise income tax slabs?

For Co-operative housing societies:

Your taxable income (from sources such as bank interest, shop rent, etc.) is taxed according to the following fixed slabs under the Income Tax Act if your housing society is registered as a Co-operative Housing Society (CHS):

- The tax rate is 10% of the total income if the total taxable income is up to ₹10,000.

- If the total taxable income is between ₹10,001 and ₹20,000, 10% tax is applied to the first ₹10,000 and 20% tax is applied to the remaining ₹10,000.

- Income over ₹20,000 is subject to 10% tax on the first ₹10,000, 20% tax on the next ₹10,000, and 30% tax on all amounts over ₹20,000.

For RWA or Apartment Owners’ Associations

For income tax purposes, your RWA or Apartment Owners’ Association is categorised as an

Association of Persons (AOP) if it is not registered as a Co-operative Housing Society.

- Income up to ₹2,50,000 is tax-free because the AOP is taxed according to individual slab rates.

- 5% tax is applied to amounts between ₹2,50,001 and ₹5,00,000.

- 20% tax is applied to amounts between ₹5,00,001 and ₹10,000,000.

- 30% tax is applied to amounts over ₹10,000,000.

(As stated in the official guidelines on AOP tax provisions published by the IT Department.)

What are the usual tax compliance requirements for RWAs?

Filing ITR and PAN (Form ITR-5)

Each RWA must obtain a PAN and file an ITR-5 annually if they have any taxable income. The ITAT (Mumbai) decision in Samata CHS Ltd vs DCIT (2025) reaffirmed this compliance, especially with reference to bank interest.

TDS on payments to contractors and professionals

If a RWA pays a professional more than ₹30,000 or a contractor more than ₹30,000 (in one payment) or ₹1 lakh (in a year), TDS must be withheld under Sections 194C and 194J, respectively.

What are the most common tax-related mistakes made by RWAs?

“We’re non-profit” justifies not filing an ITR.

A grave error. Even if you are not making a profit, you still need to declare income like bank interest or external rent.

Vendor invoices do not include TDS.

Many RWAs inadvertently fail to include TDS on large vendor payments, which leads to penalties under Section 201 of the Income Tax Act.

Putting money into nationalised banks and paying 30% less in taxes

RWAs in all states, not just Maharashtra and Gujarat, may forfeit their Section 80P benefits if they choose to invest in private or nationalised banks rather than cooperative banks. Only cooperative housing societies are affected by this, as they are the only ones that can take advantage of 80P deductions when making investments in other cooperative organisations.

Mistaking the applicability of GST for income tax

RWAs commonly make the mistake of assuming that maintenance fees that are subject to GST (more than $7,500 per flat per month) are also subject to income tax, even though this is untrue.

Not making a distinction between member and non-member revenue

Mutuality is weakened, and audit issues arise. Member surpluses are exempt, but outside income is not.

Which court decisions clarified the RWA income tax regulations?

Venkatesh Premises Co-op Housing Society Ltd. v. ITO (Supreme Court, 2018)

Problem: The Income Tax Department claimed that the society’s transfer fees and non-occupancy charges, which exceeded the amount permitted by the Maharashtra Co-operative Societies Act, qualified as taxable income.

Conclusion: The Supreme Court ruled in favour of the housing society. According to the ruling, as long as the funds are gathered from members and utilised for the good of all members, they still qualify under the mutuality doctrine even if they surpass regulatory caps. Consequently, such income is not subject to taxes.

Samata CHS Ltd. vs. DCIT (ITAT Mumbai, 2025)

Problem: The co-operative society claimed Section 80P(2)(d) as a deduction for interest earned on deposits in a co-operative bank. The Assessing Officer denied the deduction.

A ruling in favour of society was made by the ITAT Mumbai. It argued that a co-operative housing society can fully deduct interest paid from cooperative banks under Section 80P(2)(d), but not from nationalised banks. This case highlighted the importance of where excess funds are kept.

What tax distinctions exist between Maharashtra, Karnataka, Tamil Nadu, etc.?

Depending on how and where your housing society is registered, the same income (such as bank interest or transfer charges) may be taxed differently:

Maharashtra

According to the Maharashtra Co-operative Societies Act of 1960, the majority of housing societies are registered as Co-operative Housing Societies (CHS). Under Section 80P, these are eligible to receive a complete tax exemption on interest from cooperative banks. According to the Venkatesh Premises Supreme Court decision, charges such as transfer fees and non-occupancy fees are also shielded by the mutuality principle, even if they surpass caps.

Karnataka

Here, RWAs are frequently registered as AOAs under the Apartment Ownership Act or as RWAs under the Karnataka Societies Registration Act. Usually, these are handled as Association of Persons (AOPs). Unless specifically registered as a co-operative society, they are not automatically granted Section 80P exemptions. Bank interest income is subject to taxation and may be subject to tax slab rates.

The state of Tamil Nadu

The majority of flat buildings are registered as Flat Owners Associations, or AOAs, and operate in accordance with the Tamil Nadu Apartment Ownership Act. They are regarded as AOPs as well. Interest income from any bank is taxable because they are not co-operative entities, and they are not eligible for 80P deductions.

Delhi and Other Union Territories

RWAs are regarded as AOPs for tax purposes and are registered under the Societies Registration Act of 1860. No 80P benefits. All non-member income is subject to taxes, particularly bank interest.

Gujarat

Like Maharashtra, a large number of societies have cooperative registrations. Consequently, if they invest in cooperative banks, they receive the 80P benefit.

According to the Kerala Apartment Ownership Act, Kerala societies are typically registered as AOAs. Since these are AOPs rather than cooperatives, bank interest is subject to full taxation.

When does the income tax rule not apply?

Investments in cooperative banks by cooperative societies

By claiming a full deduction under Section 80P(2)(d), these can maintain their FD interest completely tax-free.

No tax on the surplus of members

As long as it originates from members and is used for the benefit of the community, retained surplus is not considered taxable profit.

Grants from the government or authorities

If your RWA receives funding from authorities for infrastructure, it is usually regarded as a capital receipt rather than income.

How ADDA Encourages Income Tax Compliance and Transparency

ADDA is more than just a community app; it is a governance platform designed to uphold your housing society’s fairness, responsibility, and compliance:

Accounting for Members and Non-Members separately

This ensures that member and non-member income is accounted for separately. Transparent ledgering is useful during audits.

All set for an audit Reports and Assistance with ITR:

Make vendor ledgers, income-expenditure statements, and balance sheets that are downloadable and compliant with ITR-5 reporting.

Paying Vendors and Tracking TDS

Automatically flag vendors who surpass threshold limits and remind treasurers of applicable TDS.

Tax Disclosure Document Repository:

Form 16A, TDS certificates, and ITR acknowledgements are available to MC and auditors.

Interaction Without Spam

Important tax updates are sent to residents through ADDA’s notification system rather than through WhatsApp or loud groups.

Click here to see all of ADDA’s Accounting and Management modules>>

FAQs Regarding Income Tax Regulations in Housing Societies

Are RWAs’ monthly maintenance fees taxable?

No. Maintenance fees paid by members are exempt under the mutuality principle.

Is a RWA necessary in order to file an income tax return?

Yes, as long as there is any taxable income, like bank account interest or rent from other sources.

What would happen if the RWA only offered interest on amounts under Rs. 2.5 lakhs?

If it is registered as a society, it can claim the basic exemption. To claim a TDS refund, it is recommended to file an ITR or maintain records.

Can RWAs be fully exempted from paying bank interest taxes?

Only when a co-operative society invests in a co-operative bank (Section 80P). Others are required to pay taxes.

Are fees for member transfers taxable?

No. The Supreme Court’s decision in Venkatesh Premises states that member fees are exempt even if they exceed the state cap.

Are vendor payments subject to TDS?

Yes. RWAs must deduct TDS in line with Sections 194C and 194J if payments exceed the threshold.

What happens if RWA does not deduct TDS?

The IT Department may treat the RWA as an “assessee in default” and pursue penalties, interest, and taxes under Section 201.